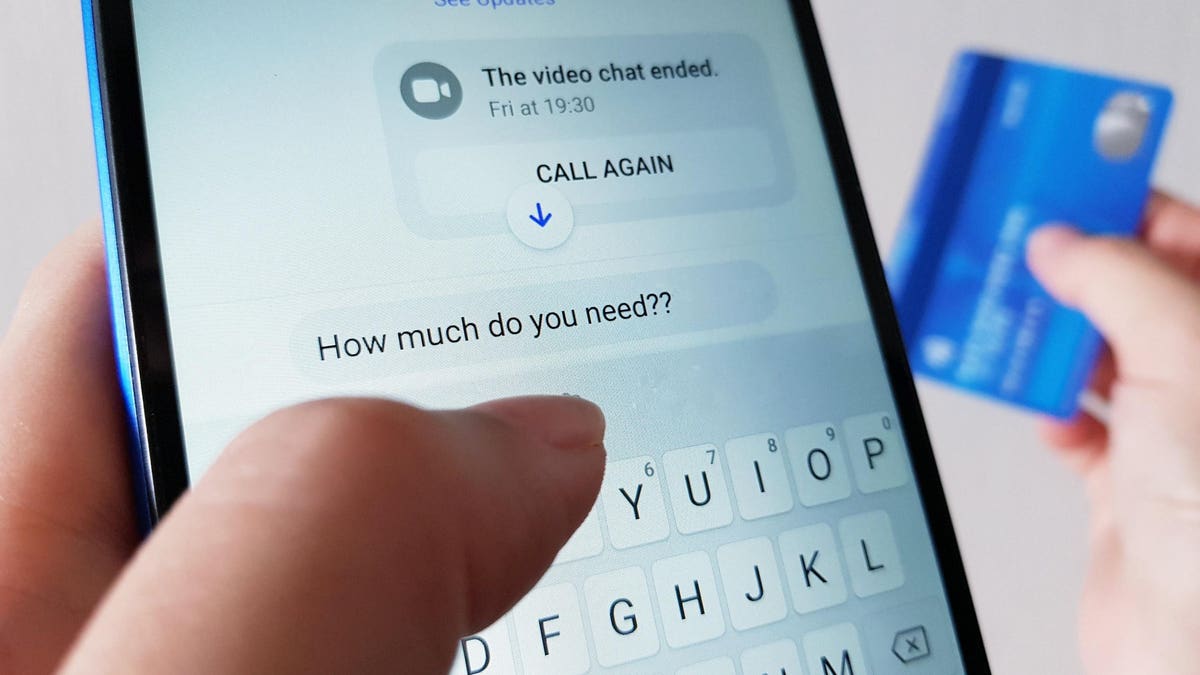

There is a very interesting argument developing in the British financial services sector at the moment, an argument that is being watched around the world wherever “authorised push payment” (APP) fraud is escalating to crisis levels (eg, Australia, where consumers lost a record amount of more than three billion dollars to scams last year). The British banks have been pushed into signing up for something called the “Contingent Reimbursement Model” (CRM) which means, essentially, that if you send money to fraudsters, the bank has to give your money back. This is unsustainable and it cannot be remedied without action on digital identity.

Just as in the US, where Zelle fraud is becoming a very serious problem, UK bank customers are losing enormous sums of money to fraudsters who trick them into sending money via instant payments. The UK’s Payment Systems Regulator (PSR

PSR

Support authors and subscribe to content

This is premium stuff. Subscribe to read the entire article.

{kind=link}