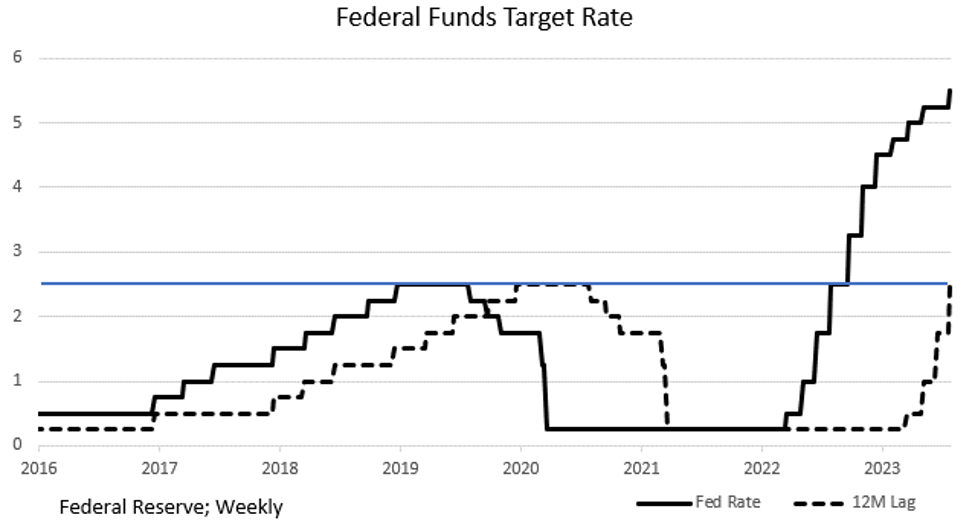

Several weeks ago, we described the effectiveness of monetary policy on the economy if it acted with a 12-month lag. The San Francisco Regional Federal Reserve Bank recently published research showing the lag to be 11 months. The Fed has also indicated that the “neutral” Fed Funds rate is 2.5%, so effective rates below 2.5% are accommodative and those above 2.5% are restrictive. In July, 2022, the Fed Funds rate was 2.5%. So, according to the SF Fed, up until June, 2023, Fed policy actually remained “accommodative.” Of course, the Fed has continued to rapidly raise rates. The economy has shown signs of weakening as the rate rises have moved toward restriction. As seen from the chart, given the lags, “restrictive” policy is about to bite, and bite hard!

From Growth to Recession

A Recession just doesn’t appear one day. It is a gradual process that takes the economy from positive to negative growth. Economist David Rosenberg, in his recent daily missives, has pointed out that in going from positive to negative growth, the economy must transition through zero growth. His conclusion is that we are close to that today, and, perhaps, that is what the “soft-landing” proponents are looking at. For us, the important question to ask, and one that is answered by our chart, is: If we have miniscule growth today, when the effective rate has just reached “neutral,” what is the likely growth path for the economy as the effective rate more than doubles over the next year? The logical conclusion: negative growth, i.e., Recession.

Support authors and subscribe to content

This is premium stuff. Subscribe to read the entire article.

{kind=link}