Onchain Highlights

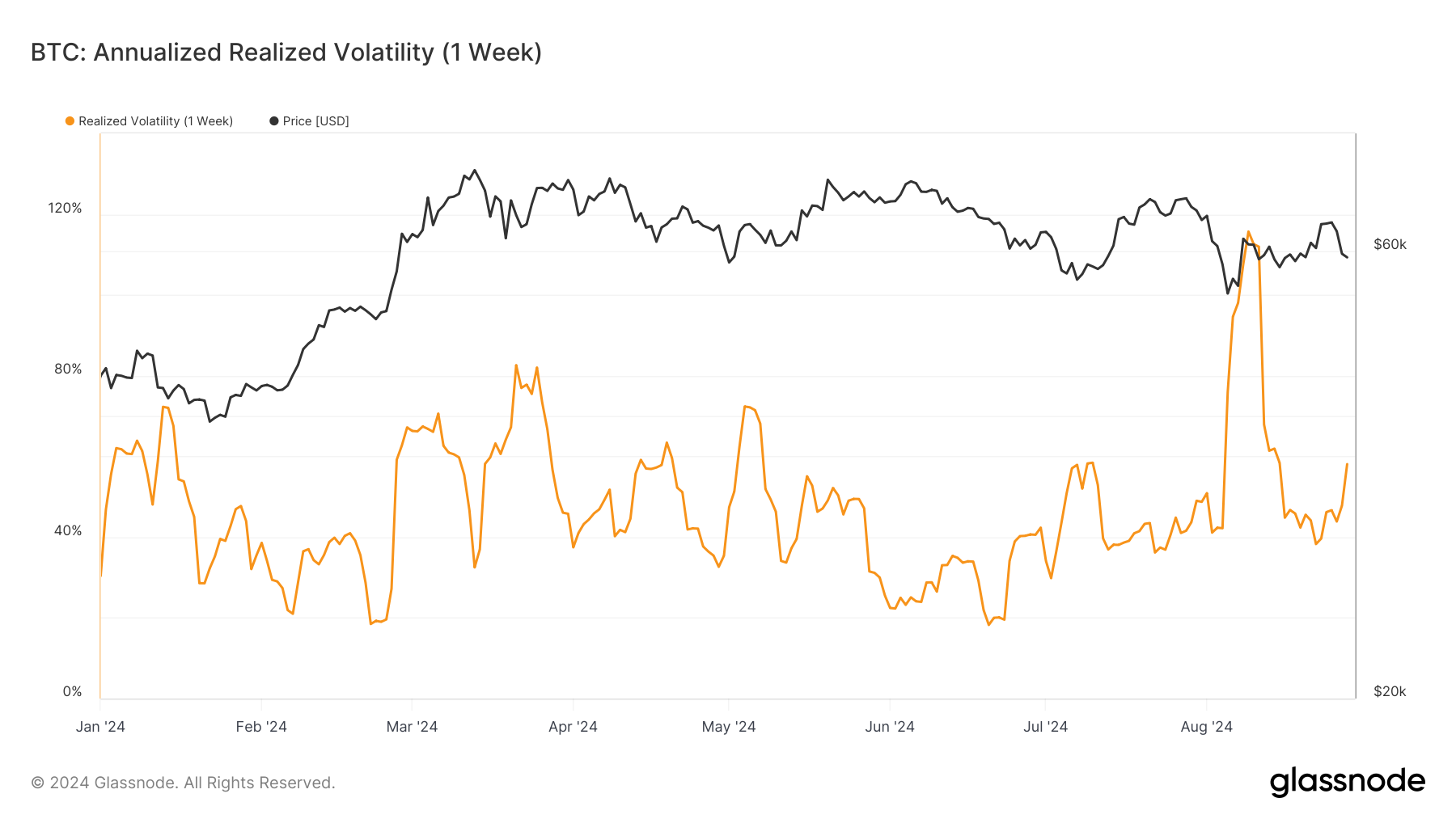

DEFINITION: Realized volatility is the standard deviation of returns from the mean return of a market. High values in realized volatility indicate a phase of high risk in that market. It is measured on log returns over a fixed time horizon or over a rolling window to obtain a time-dependent observable. While implied volatility refers to the market’s assessment of future volatility, realized volatility measures what happened in the past. Here, we calculate the realized volatility based on daily returns and multiply it with a factor of sqrt(365) to yield the annualized daily realized volatility over a rolling window of 1 week.

Bitcoin has experienced varying levels of realized volatility in recent years. The chart shows that Bitcoin’s annualized realized volatility over a 1-week window has seen significant fluctuations since 2023.

Support authors and subscribe to content

This is premium stuff. Subscribe to read the entire article.

{kind=link}