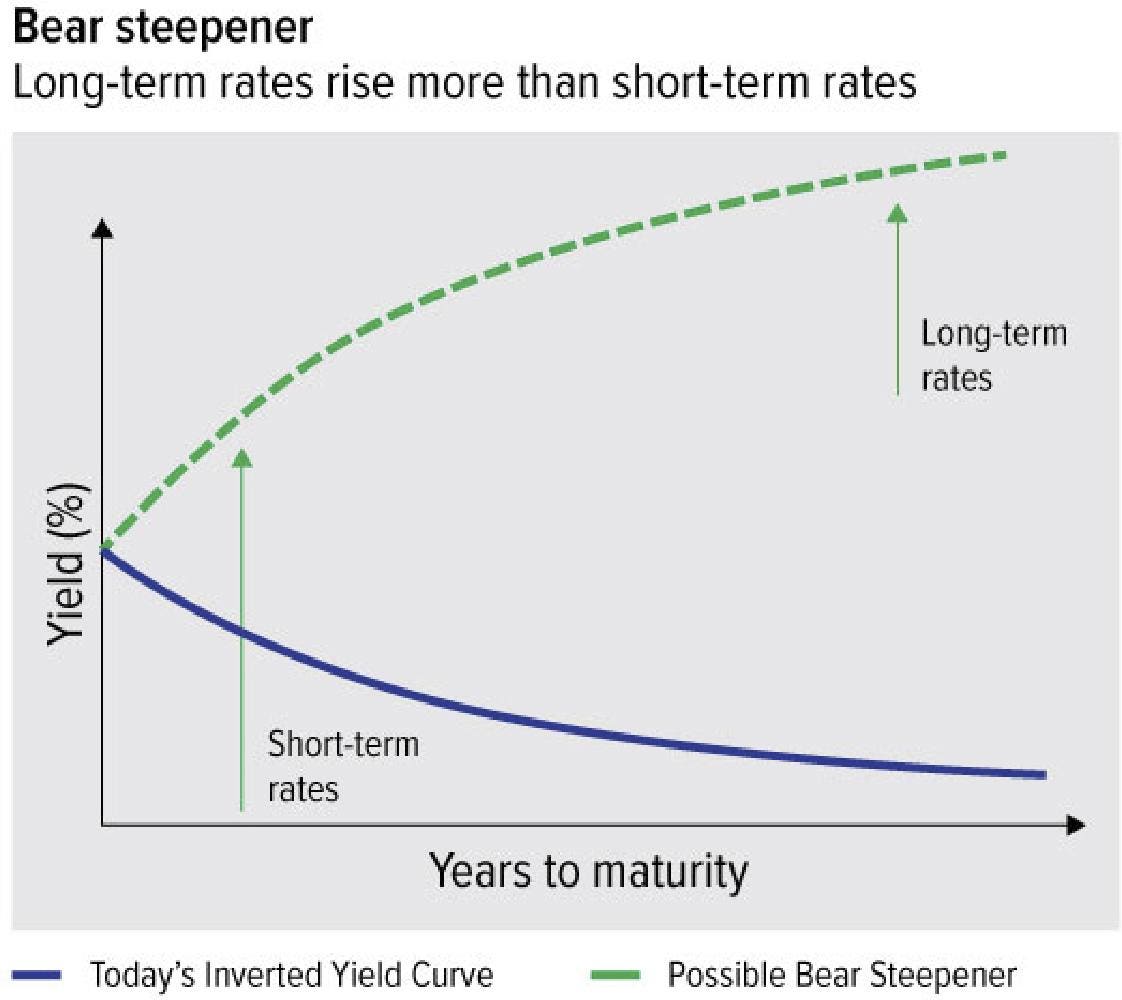

In my last missive (The Stock Market Loves Bidenomics (So Far) (forbes.com)), we pointed out a rare policy called “fiscal dominance”. Now we may have spotted another rare bird. Let’s start with a yield curve primer: The yield curve maps out interest rates (we care in this case about US Government) all the way from 3 months to 30 years. Usually, as in 90% of the time, shorter rates are lower than longer interest rates (by about 1% or more). Bond gurus call this a steep yield curve. Makes sense because a bond holder should be compensated to hold for a longer term. Occasionally, like now and since 2022, short interest rates are higher than long ones; this we call an inverted curve. Simplistically, there are two ways a yield curve can steepen: short-term interest rates go down faster than long-term rates or long-term rates go up faster than short-term rates. The latter journey is the “bear steepener”.

Protracted bear steepeners – ones that last more than a few days and move more than a few basis points – are a rare sighting in one’s career. Yet understanding how to spot one, why they occur, and what they mean for other asset classes is important. Historically, there are many times the yield curve is steepening. But is rare to get a bear steepener once the curve has become inverted. Since 1976, let’s point out the times where the curve bear steepened after it was in an inverted shape: 1980-82, 1990, 2001, 2007, and 2020. That is a royal flush of recession warnings, ugh!

Support authors and subscribe to content

This is premium stuff. Subscribe to read the entire article.

{kind=link}